Barron's Cover

U.S. Money Managers Turn Cautious

Money managers have reined in their optimism since the fall, but they see bargains in Europe, energy, tech.

By Jack Willoughby

April 25, 2015

America’s money managers have developed a fear of heights. Doctors might call it acrophobia, but investors call it a logical response to a stock market that has more than doubled in the past six years, and now sits just below an all-time high. This widespread wariness is evident in Barron’s latest Big Money poll, in which a record 50% of respondents categorize themselves as neutral about the market’s prospects through year end. That’s the highest neutral reading since the spring of 2005, when 40% were sitting on the fence, and a sharp increase from last fall’s 31%.

“We see more tentativeness than we did last year, and more withdrawal requests,” says Douglas MacKay, founder of Broadleaf Partners in Hudson, Ohio, with $170 million under management. “There’s just not that urgency to get in. Your average investor isn’t putting money into stocks.”

Our poll would seem to confirm as much, with 65% of managers saying that their clients are neutral on stocks, and 10% indicating they’re bearish. Chris Wang, director of research at Runnymede Capital Management in Morristown, N.J., which oversees $200 million, thinks he understands why. Wang considers himself bullish, and believes that expansionary monetary policies, corporate mergers, and share buybacks could propel stocks higher still. “But investors have reason to be cautious,” he says. “This is the sixth year of a bull market. Is the economy slowing? How soon will the Federal Reserve raise interest rates? These are questions that worry investors.”

The market’s valuation is also a concern. Seventy-one percent of Big Money managers say that stocks are fairly valued, while just 8% consider them undervalued. The Standard & Poor’s 500 is trading at 17.4 times this year’s expected earnings of $121.17, on the high side relative to its history.

While Wall Street analysts expect S&P profits to rise less than 1% this year, according to Thomson Reuters, the Big Money managers aren’t entirely pessimistic. Seventy-four percent expect earnings to increase by 1% to 5%, and 25% peg growth at 6% to 10%. Just 36% of poll respondents look for the market’s price/earnings ratio to expand in 2015, compared with 45% who see no change, and 19% who forecast multiple compression.

Robert Maynard, chief investment officer of the $15 billion Public Employee Retirement System of Idaho, or Persi, calls the market “fully valued to slightly overvalued, but not stunningly so.” He expects a combination of economic growth, stock buybacks, and dividends to produce a total return of 9% this year, or 7% on an inflation-adjusted basis.

THE BULLS’ CAMP is home to 45% of Big Money managers this spring, about on par with the spring of 2007, but down from 59% last fall. Based on their mean prediction, the bulls expect the Dow Jones industrials to rally about 4% through the middle of 2016, ending this year at 18,824, en route to 19,531. The S&P 500 similarly could tack on 8%, they estimate, hitting 2282 by June 30, 2016, while the Nasdaq Composite could add almost 7%, to 5382.

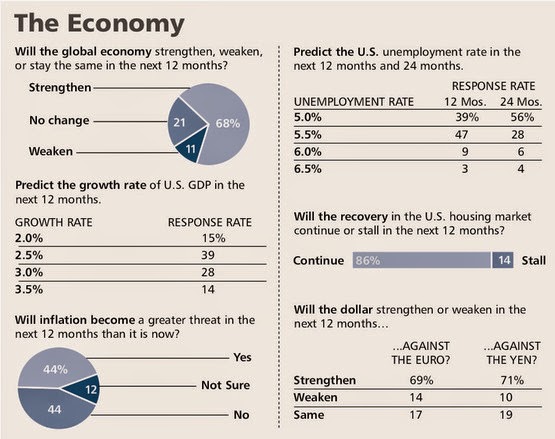

Most poll respondents are upbeat about the global economy, with 68% expecting the recovery to strengthen in the next 12 months. They look for continued growth in the U.S. economy, with 39% predicting a 2.5% increase in gross domestic product, and 42% putting GDP gains at an annualized 3% or 3.5% in the year ahead. Fourth-quarter GDP increased at an annualized rate of 2.2%; the Commerce Department will release first-quarter numbers on April 29.

Consistent with their rosier economic outlook, most Big Money managers expect an unemployment rate of 5.5% to 5%, just about half the level in 2009, in the aftermath of the financial crisis. Eighty-six percent expect the three-year-old housing recovery to continue. The housing market sent conflicting signals last week: The National Association of Realtors reported that existing-home sales rose 6.1% in March, to the highest level in 18 months, while the Commerce Department said that new-home sales fell 11.4% that month, the biggest drop in more than 18 months.

“We believe there is more juice left in the U.S. economy, and we expect it to push stock prices higher,” says Kaleialoha Cadinha-Pua’a, president and CEO of Honolulu-based Cadinha & Co., which oversees $1 billion. “The U.S. stands to deliver 3.5% GDP growth,” she adds, calling it a “safe haven” for investment assets in an increasingly risky world.

Company-specific developments, from mergers and spinoffs to buybacks and dividend hikes, also encourage the bulls. “A lot of things going on in the market give me comfort,” says David Marcus, co-founder of Evermore Global Advisors in Summit, N.J., which manages $400 million. “Big companies in the U.S. are transforming their operations, breaking up and spinning off new businesses, and focusing on their best businesses.”

Marcus, the survey’s most bullish respondent, puts the Dow at 24,700 by mid-2016, and the Nasdaq at 6,125. Lower fuel costs mean lower operating costs for companies—another plus, he says.

Robert Turner, chairman of Turner Investments in Berwyn, Pa., which manages $1 billion, has been bullish for several years and sees no reason to rein in his optimism. “To have a severe correction, you need severe excesses, and I just don’t see them,” he says. “Stocks trade at a reasonable multiple of expected earnings. Even the yield on the S&P 500 is on par with the yield on the 10-year Treasury, which doesn’t happen often.”

The S&P is yielding 1.96%, compared with the 10-year Treasury’s 1.99%.

Turner favors the work of Dan Wantrobski, a technical analyst at Janney Capital Markets in Philadelphia, who says “the expansion cycle” has much further to run. Demographics, he notes, point to a coming boom, as the 90 million members of the millennial generation approach family-formation age and start looking to buy and furnish homes. Moreover, the stock market typically has peaked at P/E multiples much higher than today’s, Wantrobski says.

THE BIG MONEY managers are most bullish about the prospects for European and U.S. stocks, and real estate. They are mostly bearish on U.S. Treasuries, U.S. corporate bonds, and commodities. More than 70% expect equities to be the best-performing asset class in the next 12 months, while 13% think that real estate will lead the pack.

The managers see the biggest investment opportunities in energy, European, and technology stocks, and the greatest risks in bonds, biotechs, and emerging-market stocks. They expect consumer cyclicals, health care, energy, financials, and technology to perform best among S&P 500 sectors, although, to be fair, a fourth of the managers look for energy stocks to bring up the rear.

The Big Money pros see little change in oil prices this year; their mean forecast for West Texas Intermediate crude, the U.S. benchmark, is $54.45 a barrel, compared with a recent spot price of $57.74. Gold, too, has relatively few fans in this crowd, with poll respondents looking for the metal to end the year around $1,170 an ounce, below last week’s $1,178.

Nearly half of the Big Money managers say Europe will be the best-performing stock market in the next 12 months—and that’s after European shares, as measured by the Stoxx Europe 600 index, have rallied 20% this year, in tandem with the European Central Bank’s $1 trillion bond-buying program.

Marcus, of Evermore, notes that the euro’s collapse in the past year, relative to the dollar, is bringing an export advantage to European multinationals.

The common currency slid from $1.39 in May 2014 to $1.07 last week, and 70% of Big Money managers expect the downward trend to persist.

Jason Norris, executive vice president of research at Portland, Ore.–based Ferguson Wellman Capital Management, with $4.2 billion in assets, says he has been scouring European markets for bargains. “U.S. markets have outperformed global markets by 70% these past few years,” he says. “Investors expect some reversion to the mean. Easy money in Europe promises higher equity prices, [whereas] the U.S. is on the verge of tightening monetary policy.”

The valuation differential also is a draw, he says, noting that European equities trade for roughly 15 times expected earnings.

BARRON’S CONDUCTS the Big Money poll every spring and fall, with the help of Beta Research in Syosset, N.Y. The latest survey, e-mailed in late March, drew responses from 143 money managers across the country, representing some of the nation’s largest investment firms and pension funds, as well as many smaller investment boutiques.

What might send U.S. stocks sharply higher in the next 12 months? Nearly half of the managers cite rising corporate profits, while 22% point to a lack of action by the Federal Reserve. Most Big Money managers expect the central bank to begin raising short-term interest rates in the fourth quarter of 2015 or first-quarter 2016—a view that much of the rest of Wall Street also has adopted in the past month, based on recent, less-than-stellar economic reports. This will mark the first change in the Fed’s rate target since December 2008, and the first increase since June 2006.

Only 25% of respondents expect the stock market to slide in the six months following the Fed’s tightening, while 55% predict that stocks will rise. A majority of managers predict that the 10-year Treasury bond will yield 2.5% or 3% a year from now, although 27% see little change from today’s near-2%. Looking out five years, however, more than 40% expect the 10-year to yield 4% or more.

With interest rates at historic lows—and government bond yields negative in key European markets—the managers are split as to whether their fixed-income portfolios will generate positive returns this year. Fifty-six percent say that the U.S. bond market is exhibiting bubble characteristics, although that doesn’t mean a correction is near. “There is a bond bubble unless the Fed says otherwise,” one manager said in write-in comments. “If the Fed continues to suppress yields, there is no bubble. If the Fed does what it should, bond prices will fall as fast as the Fed will allow.”

Interest-rate suppression will end, “but the start date has been pushed out, and many now believe the process will take longer than originally expected,” wrote poll respondent John Boland, a principal with Maple Capital Management, a $650 million-in-assets firm in Montpelier, Vt., in a recent newsletter.

Boland describes a difficult backdrop filled with “troubling disconnects.” Corporate profits are going down, he notes, but people are calling for stock prices to go up. At the same time, the flow of earnings news could bring more stock-price volatility. Boland, who labels himself neutral, looks for the Dow Jones industrials to hit 18,750 by year end, but retreat to 17,000 in the first half of 2016.

A MERE 5% of the Big Money men and women are self-described bears today, down from 10% six months ago. The higher the market has climbed, it seems, the more ambivalent erstwhile bears have grown.

While more than 75% of the managers think stocks will correct by at least 10% in the next 12 months, most likely driven lower by a geopolitical crisis or earnings shock, the bears are a class apart:

They don’t see a rebound thereafter. To the contrary, they expect the Dow to slide 7% by the middle of next year, to 16,788. The S&P 500 could fall 8%, to 1935, in that span, they say, and the Nasdaq could give up 8%, to 4633.

“We look for negative returns in the coming months,” says David Villa, chief investment officer of the $105 billion State of Wisconsin Investment Board. “We’ve had a really strong run in the U.S. All the talk of rates going up at the end of the year will reverse momentum.” Villa asserts that U.S. equities are 10% overvalued, while European stocks are attractive. “For example, we really like European grocers, but find North American grocers’ shares unattractive,” he says. Villa expects the Dow to tumble to 17,250 by year end, but rebound to 18,630 in the first half of 2016.

Ralph Segall, a principal with Chicago-based Segall, Bryant & Hamill, with $9.7 billion under management, projects the Dow will fall as low as 16,800 by the end of this year, and climb back to 17,500 by June 2016. The selloff could be driven by earnings disappointments and the expectation of higher interest rates, he says. Segall sees particular risk in passive investment products, such as index funds and exchange-traded funds, which have garnered huge popularity in the bull market. They could quickly lose ground as the market grows more volatile.

“The public and institutions sound as convinced about the virtues of indexing as they did about the virtues of tech investing at the height of the bubble,” he comments. “It will all end badly, I fear.”

DESPITE THEIR concern about the market’s advance to rarified heights, the Big Money pros find plenty of stocks to like. Their top picks this spring include Apple (ticker: AAPL), Dow Chemical (DOW), American Airlines Group (AAL), Celgene (CELG), and General Motors (GM), among others.

{kind=link}

Dow Chemical shares have been relatively flat for the past year, and recently closed at $51. But David Becker, president of Northern Oak Wealth Management in Milwaukee, which manages $630 million, has a $60 target price. He expects earnings per share to rise 20% in 2016 and 2017, and lauds management’s efforts to shift to higher-margin, noncyclical businesses from commodity chemicals.

Dow pays an annual dividend of $1.68, and yields 3.33%. The company also has a buyback program.

Technically, says Becker, the stock is breaking out of a consolidation phase that lasted more than a decade.

Technically, says Becker, the stock is breaking out of a consolidation phase that lasted more than a decade.

As much as investors like dividend payments—Dow Chemical’s have been on the rise for the past four years—they also see other compelling uses for corporate cash. For example, 35% of Big Money respondents think capital spending is the best use of corporate cash today, and 11% favor acquisitions. That compares with 34% who regard dividend payments as the best investment, and 20% who prefer buybacks.

The managers see a lot of froth in biotech stocks, but Celgene, a $95 billion-market-cap giant, could be a smart way to play the industry’s rapid growth. Spun out of chemical maker Celanese in 1986, Celgene is best known for cancer treatments, and has one of the broadest pipelines in the biotech business. The company bought a number of small biotech outfits, and shareholder-friendly management has actively repurchased shares.

At a recent $116, Celgene trades for 19 times next year’s expected earnings of $6.32 a share. Geoffrey Porges, an analyst at Sanford C. Bernstein, has a price target of $155 a share, and says the stock is “set up nicely to rally.”

GM is a favorite of William Harnisch, president of Peconic Partners, which oversees $533 million in assets. The auto maker’s shares are trading around $36, or for a well-below-market valuation of seven times estimated 2016 earnings of $5.17 a share. Harnisch thinks the stock is worth at least $50, and says the market has yet to see past the company’s recent recall problems.

Nor do investors understand just how well GM is doing in truck manufacturing, he adds. In many ways, Harnisch says, GM is a stealth technology company, and a leader in computer-enhanced “connected” vehicles designed for superior performance and safety.

Robert Medway, a principal in New York’s Royal Capital Management, which manages about $100 million, prefers lesser-known stocks, and says relatively high valuations have forced bargain hunters to move into “special situations and orphan stocks that trade down because of some basic misunderstanding or disagreement.”

McDermott International (MDR), an oil-infrastructure specialist, is one example, he says. The stock was hit most recently by the plunge in oil prices, but the company has stable long-term contracts with prime producers, Medway notes.

ASK ANY GROUP of people what they think of Apple, and opinions of its products and stock will be mixed. While 81% of Big Money respondents view the company favorably, and some call its stock a favorite, others label the shares among the market’s most overvalued.

The managers also consider Tesla Motors (TSLA), Amazon.com (AMZN), Facebook(FB), and the casual-dining chain Chipotle Mexican Grill(CMG) to be among the market’s most overvalued names, as they did last fall, even though Tesla and Chipotle have fallen 4% and 1% since late October, and Facebook is up 9%. Amazon is another story; it’s up 28% in the past six months, to $390, and fetches a cool 165 times next year’s expected earnings.

Chipotle trades for a comparatively reasonable 31 times estimated profits, but that is too rich by far for James Pappas, chief investment officer of James Pappas Investment Counsel, which manages $30 million in Longboat Key, Fla. “This is not a cure for cancer; it is a burrito chain whose growth is starting to slow,” he says.

Pappas notes that Chipotle’s $19.7 billion stock market capitalization values each of its 1,800 stores at a lofty $12 million. The restaurants produce an annual profit of $250,000 each. Viewed another way, that’s just a 2% return, akin to the 10-year Treasury yield, but with a lot more risk.

Pappas expects the Dow to hold steady for the rest of this year at about 18,000, before climbing to 19,200 by mid-2016—an implied gain of just under 7%.

POLITICS ARE HARD to escape these days, even if you try. What happens in the Capitol, and on the hustings, is of keen interest to the nation’s investment managers, especially given Washington’s growing influence on Wall Street. If the Big Money folks could write the script, 39% would like to see the White House and Congress focus most urgently on tax reform, and presumably on lowering the nation’s corporate tax rate.

Another 29% argue that reform of entitlement programs is the top priority, while 11% contend it is reductions in federal spending. Only 6% consider immigration reform the most pressing issue before Congress.

At this early juncture, 79% of Big Money managers expect Hillary Clinton to be the Democrats’ candidate for president in 2016. Just half of poll respondents think Jeb Bush will carry the banner for the Republicans, with another 20% putting high odds on Wisconsin Gov. Scott Walker. No matter who runs, 66% predict that the Republican candidate will win.

The markets could look a lot different—or not—by the time the next president reports for duty. In the meantime, the nation’s professional money managers have their work cut out, especially given stocks’ valuation and the uncertainty surrounding the Fed’s next rate move. Eighty-two percent of Big Money managers say they’re beating the market this year—a good batting average. We’ll let you know how they’re doing, and what they’re thinking, when we check back with them in the fall.

0 comments:

Publicar un comentario